Breaks in pricing based on loan limits is actually not too confusing. Understanding it isn’t difficult. Finding it explained well online is it seems. Let’s break that mold.

No matter what the loan program, there are three types of limits;

- Baseline Conforming

- High Balance

- Jumbo

Generally loans becomes more expensive at each tier. The limit where you are is based on the county you are in, relative to the value of the homes in the area. In some areas of California the Baseline Conforming limit is the same as the High Balance limit. In some the High Balance limit is quite a bit higher. When a loan amount exceeds the county’s High Balance limit the loan is considered a Jumbo. The government will purchase loans from a lender up to a county’s High Balance limit, but they won’t buy a Jumbo. Most lenders have their own network of private investors that fund their Jumbo loans. Rarely these days do lenders portfolio or keep a loan once it is funded. They often keep the loan servicing, meaning you still receive a mortgage statement from them, but they no longer own the loan itself.

So enough bank politics. What are the limits?

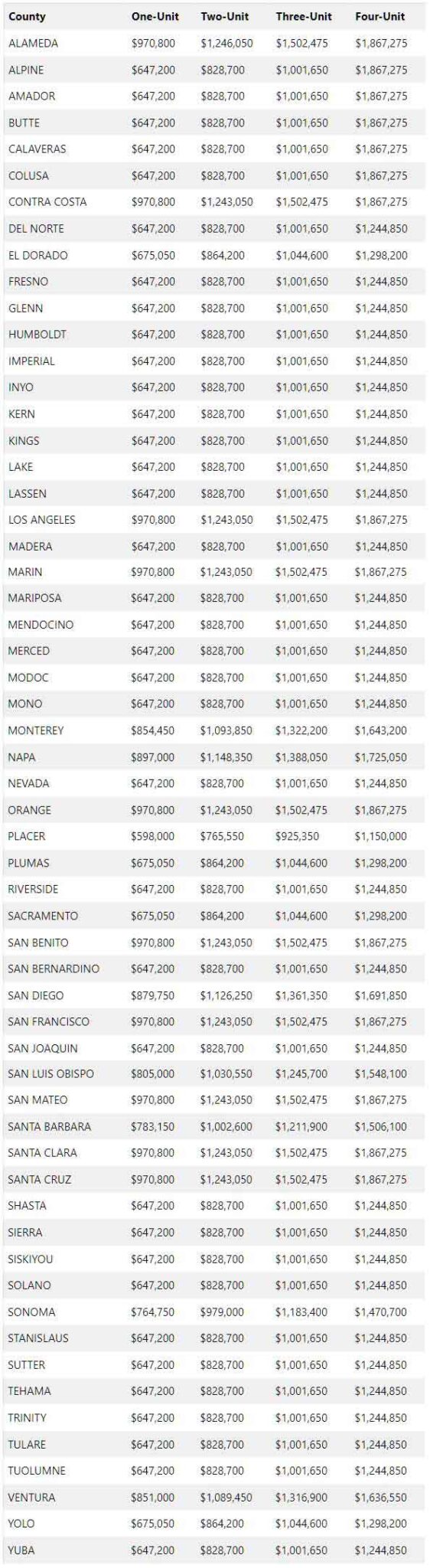

- Baseline Conforming – In November 2021, the Federal Housing Finance Agency (FHFA) announced that they were raising the 2022 Baseline Conforming loan limit in California to $647,200.

- The FHFA also raised the 2022 High Balance loan limits in California. The chart below shoes the High Balance limits throughout California.

- Jumbo – Any loan placed on a residential property which is above the High Balance limit for that particular county is considered a Jumbo loan.

Here are the High-Balance limits in California for 2022: